2026 Economic and Investment Outlook

Staying the Course: Discipline in a High Valuation Market

1Q2026

From the Innovest Investment Committee

The Year in Review: 2025

In 2025, capital markets sustained their upward march and concluded a third straight year of impressive gains. Three themes shaped the strong rally in global markets: domestic equities kept climbing despite valuations surpassing 20 year averages; AI headlines continued to drive domestic markets, with Google (GOOGL) up ~66% in 2025; and international companies in both developed and emerging markets ended the year up over 30% compared to the S&P 500’s 17.8%. Each of these themes—the risk of high valuations, the uncertainty of AI, and the reversal of domestic equity dominance—have tended to reward investing that is patient, disciplined, and diversified.

Equities - As domestic equities round out a third year of double-digit performance across market capitalizations, many investors have rightly expressed concern over ballooning equity valuations. Some hear echoes of the dot-com bubble’s irrational exuberance in the AI-heavy rhetoric that saturates today’s headlines and earnings calls. While there are certainly similarities between now and the early 2000’s bubble, the Price-to Earnings (P/E) ratios of top companies are starkly different. In October, Goldman Sachs reported that the median 24-month forward P/E ratio across the Magnificent 7 is 27x, which is roughly half of the equivalent valuation of the largest 7 companies during the dot-com era. Even so, domestic valuations are higher than they were a year ago and hover near the top of their 20-year range. We recommend staying in the market while maintaining prudent geographical diversification and disciplined rebalancing to ensure that portfolio risk stays in line with investor tolerance.

Fixed Income and the Fed - The Federal Reserve (the Fed) cut interest rates three times in 2025, boosting fixed income portfolios, with the Bloomberg U.S. Aggregate Bond Index returning 7.3% for the year. Although inflation remains above the Fed’s target, Chair Jerome Powell has advised that these cuts are intended to support a weakening labor market. In 2025, the U.S. added an average of 49,000 jobs a month, down from 168,000 per month in 2024. This makes 2025 the worst year for job creation outside of a recession in more than two decades. However, GDP growth remains strong and increased tariff revenue has helped to decrease the federal deficit relative to last year. Looking forward, guidance from the Fed’s Summary of Economic Projections indicates that the median committee member expects the Federal Funds rate to be 3.4% at the end of 2026 and 3.1% at the end of 2027, potentially signaling one rate cut in each of the next two years.

Diversifiers – Diversifying asset classes delivered robust performance over the course of the year, providing stable, consistent returns that were relatively uncorrelated to stock and bond markets. Hedge funds and infrastructure real assets were the standout, both delivering high single digit or low double digit returns with minimal volatility. As an asset class, these strategies continue to play a key role in portfolios by enhancing diversification and contributing to a more balanced risk/return profile, particularly in periods of higher volatility.

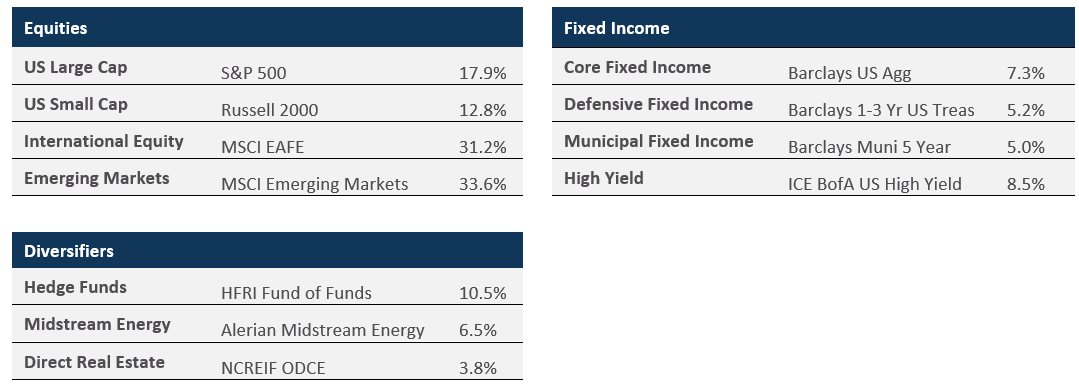

Chart 1: Calendar Year 2025 Returns

Sources: Morningstar and Innovest Portfolio Solutions. As of 12/31/2025.

2026 Capital Markets Outlook

As we turn our focus to 2026, we expect to see heightened geopolitical tension that may have ripple effects across global markets. Broadly speaking, we are wary of the high domestic equity valuations and declining fixed income yields, and so we have slightly reduced our return expectations across all asset classes, with the exception of real estate. There are a multitude of risks to both the upside and the downside, including the lingering impact of tariffs, the effects of the One Big Beautiful Bill tax code changes, a weakening labor market following decreased immigration, and high concentration in AI tech stocks making the economy more susceptible to shocks in that sector.

The markets have generally digested the uncertainty of trade and tariff policy along with the potential ramifications of the passage of the One Big Beautiful Bill. Nonetheless, there are always unknown surprises from a global, macro-economic perspective.

Ballooning valuations create a higher-risk environment. U.S. equity valuations remain stretched compared to long term historical averages, while international equities look more appropriately valued. Investors should remain diversified by geography, capitalization, and style.

Although yields have declined, fixed income remains attractive and continues to act as a ballast in diversified portfolios. Continue to favor active management over passive management in fixed income.

Recent declines in real estate valuations may provide an attractive entry point. A pickup in overall growth should lead to higher rents and property valuations.

Infrastructure spending continues to accelerate, reaffirming our outlook on the asset class.

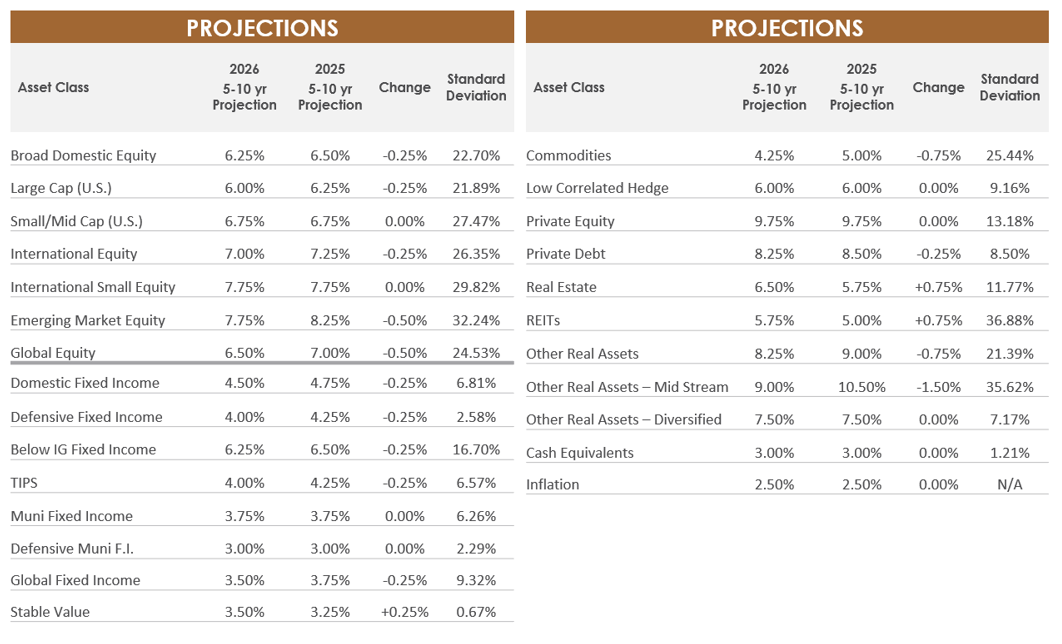

Chart 2: Long Term Capital Market Projections

Portfolio Construction

When revising our forward-looking assumptions and evaluating portfolio construction, our primary focus is to build the best portfolios for our clients. Rather than attempting to predict interest rate movements or market fluctuations in the short term, which we believe is a fool’s game, we emphasize the importance of reassessing return objectives and understanding the risks embedded in portfolios over an extended time horizon.

Our primary emphasis remains on constructing custom portfolios and employing regular rebalancing to help maximize the probability of meeting long-term goals. We continue recommending that our clients maintain diversification and have exposure to asset classes that do well in a variety of economic scenarios, ensuring resilience amid an evolving market landscape.

Equities – Proceed with Caution

The S&P 500 gained ~18% in 2025 with the “Magnificent Seven” stocks once again leading the way, fueled by favorable investor sentiment and sustained capital investment into AI. Beyond U.S. borders, developed international and emerging market equities appear more attractively priced even despite their stellar year, with valuations abroad still attractive compared to valuations at home. Although small- and mid-caps have begun to join the large cap party, an even wider-spread participation in the equity rally would still be a welcome outcome for 2026.

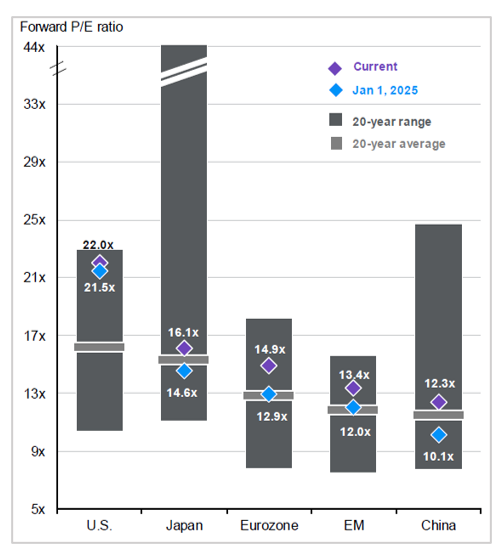

Chart 3: Equity Valuations

Sources: FactSet, MSCI, Standard & Poor’s, and J.P. Morgan Asset Management. As of 12/31/2025.

Global Equity Valuations

Despite elevated valuations in the U.S., AI headlines, and ongoing geopolitical risks, equities remain a cornerstone of portfolios, offering long-term capital appreciation and a hedge against higher inflation. We continue to emphasize the importance of diversification across size, style (value or growth), and geography.

Fixed Income – A Return to Normal?

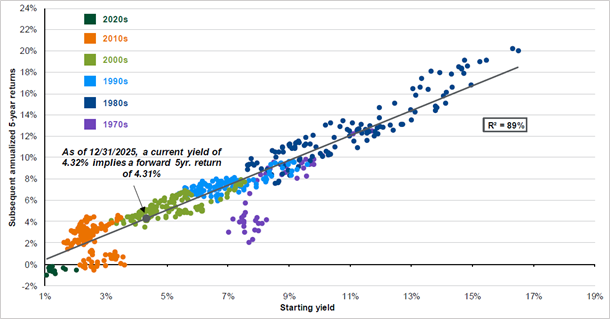

Although fixed income markets had a strong year, current fixed income yields indicate that there is still a good runway for future returns. A more normalized yield curve has developed, with short-term rates falling below longer-term rates. This dynamic, combined with the potential for rate stabilization, positions fixed income as an appealing low-volatility option.

Although the cutting cycle has slowed, fixed income remains an attractive diversifier for many portfolios. While rate cuts provide a short-term boost to bond performance, a stabilization of rates above the 2010s near-zero level provides a steady base of income to bond performance. Continued normalization of the yield curve provides a potential tailwind for duration, enhancing the attractiveness of longer-term bonds for income generation and potential capital appreciation in a shifting market environment.

Chart 4: Fixed Income Yields and Forward Returns

Sources: Bloomberg, Factset, and J.P. Morgan Asset Management. As of 12/31/2025.

Nuances of U.S. Concentration – U.S. Growth Remains a Global Story

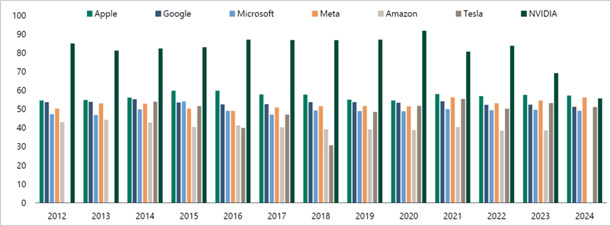

While it is undeniable that there are major risks associated with S&P 500’s high concentration in the Magnificent Seven, the broader concentration narrative is more nuanced than it may first appear. Each of these seven companies are global in their customer base and operations, and most of them derive around 50% of their revenue from abroad. Although there are certianly company specific risks that are more dangerous due to S&P concentration, geographic risks may be less elevated than many investors fear.

Chart 5: Percent of Revenues from Abroad for the Magnificent 7

Sources: Bloomberg, Apollo, Apollo Chief Economist. Data as of 12/31/24.

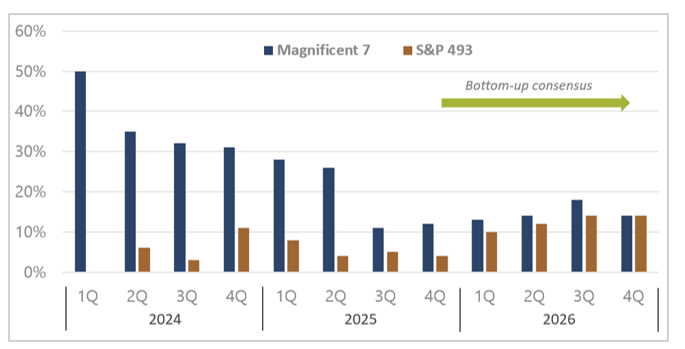

Equity Analysts Predict a Broadening of Performance Beyond the Magnificent Seven

Chart 6: Robust Earnings Growth for S&P 493

Source: Goldman Sachs, Aptus Capital Advisors. Data as of 8/15/25.

Earnings growth for the S&P 493 (representing the S&P 500 without the Magnificent 7) has recently been showing signs of strength. Equity analysts across Wall Street are forecasting a normalization of Magnificent 7 earnings growth and increased participation from the rest of the index. Such an outcome would reward investors who are diversified across more than just the largest technology companies.

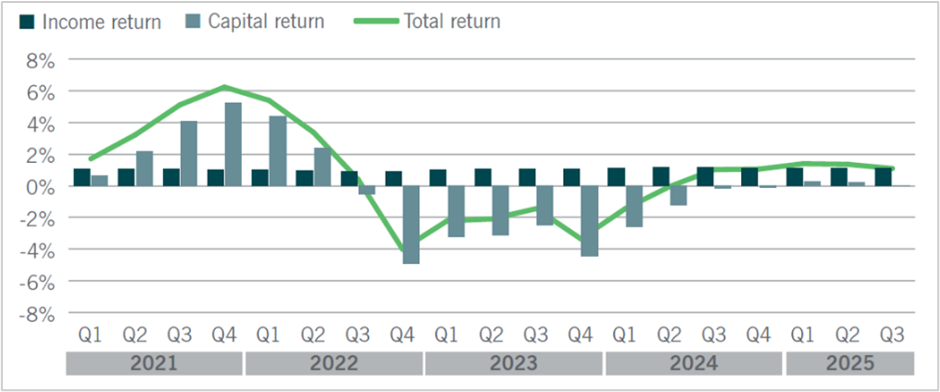

Opportunity in Real Estate

Chart 7: Quarterly ODCE Returns (2021 to 2025)

Source: ODCE refers to Open-end Diversified Core Equity (ODCE) private commercial real estate. Nuveen, NCREIF ODCE. Data as of 9/30/25.

The broad property value decline in 2022 and the beginning of 2023 has begun to stabilize, potentially signaling the beginning of a new cycle. Property values in Europe and Aisa are rising, and it seems likely that the United States will follow. We believe that managers who can create value and increase income at the property level will benefit from fundamental tailwinds in the years to come.

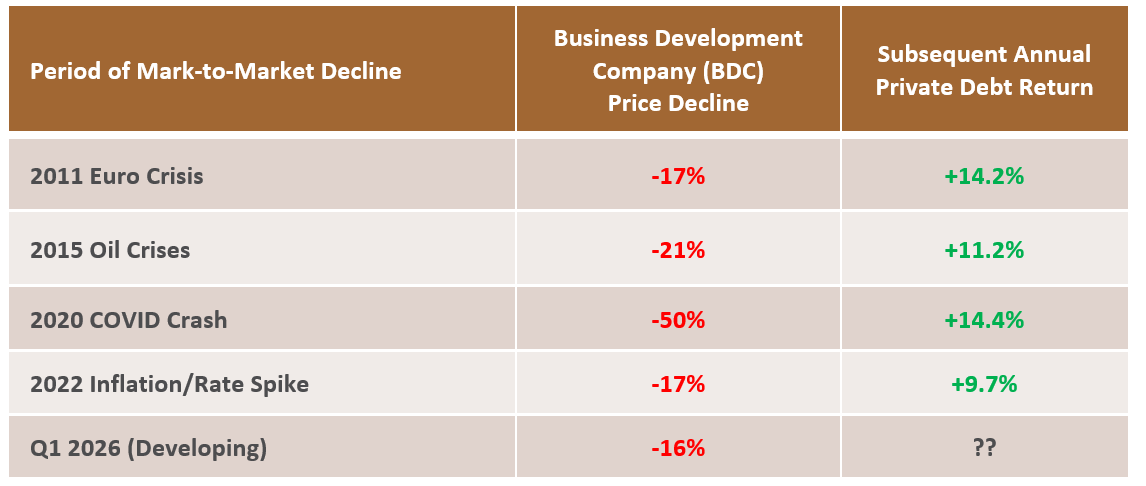

Media Spotlight on Private Credit Underscores the Need for Thoughtful Diligence

Narrative-driven articles in the financial press have recently raised concerns that private debt vehicles offered to the public may be over-levered, potentially contributing to liquidity risks. These articles fail to clarify a critical distinction: exposure to private credit is not just a bet on an asset class; its outcomes are a function of the specific fund structure and the manager’s execution. While there are real issues to monitor in specific credits, we believe broad credit metrics remain in line with or better than historical averages. When it comes to manager selection, we prefer to stay away from the broadly syndicated loan market with its high leverage and stiff competition, and instead prefer the direct lending market with loans that are primarily senior secured and private-equity sponsor backed, managed in a structure that keeps both fund-level and look-through leverage well under 1.0x.

The recent media hysteria concerning mark-to-market (M-T-M) decline should be taken with a grain of salt. M-T-M declines primarily reflect market sentiment and interest rate volatility and are not necessarily reliable indicators of the fundamentals behind the underlying credits. Investors should instead look to loan defaults and credit losses to better understand the current state of credit markets. In past periods of high M-T-M declines amongst Business Development Company (BDC) vehicles, subsequent annual returns for the overall private credit markets were very strong. History shows that direct lending has a long track record of weathering volatility well, provided the manager is disciplined and the vehicle structure is sound.

Chart 8: Private Debt and BDC Historical Performance

Source: Cliffwater, Preqin, FRB, Haver Analytics, Apollo Chief Economist. BDC price discount as measured by the Cliffwater BDC Index (CWBDC), Private debt represented by Cliffwater Direct Lending Index (CDLI). Data as of 2/20/26.

Navigating Uncertainty through Diversification

As we enter 2026, financial markets are navigating a shifting economic landscape marked by geopolitical conflict and uncertainty for the future. While inflation remains modest and GDP growth is relatively strong, the lagged effects of 2025 tariff policy and One Big Beautiful Bill tax implications remain to be seen. Growth in developed markets is expected to slow, but recession risks appear contained, bolstered by strong household and corporate balance sheets.

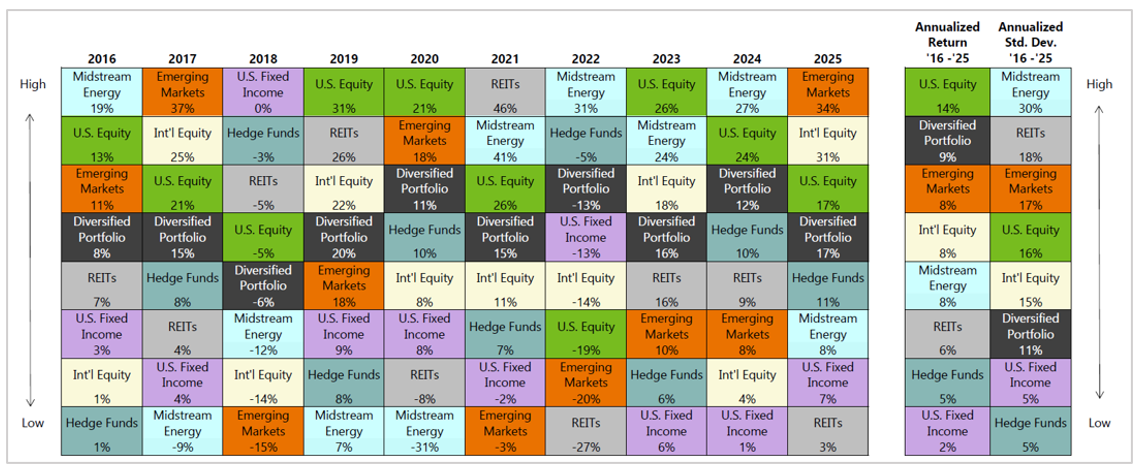

Chart 9: Periodic Table of Returns (2016-2025)

Sources: Morningstar and Innovest Portfolio Solutions. As of 12/31/2025.

Diversification remains paramount as elevated U.S. equity valuations and concentrated performance among a few sectors may create potential headwinds and downside risks. Fixed income offers a compelling opportunity, with higher yields providing better income generation in this decade than the prior decade and enhanced portfolio balance. By allocating to asset classes positioned for a variety of economic scenarios – growth, inflation, economic slowdown, etc. – investors can better navigate the challenges of an evolving market environment.

Predictions often fail to account for the surprises that truly matter. In an environment marked by uncertainty, disciplined portfolio construction, prudent risk management, and a commitment to long-term diversification are essential to achieving sustainable outcomes. A forward-looking approach that embraces these principles enhances resilience and maximizes the likelihood of meeting client objectives.

Disclosure

Innovest is an independent Registered Investment Adviser registered with the Securities and Exchange Commission. The material herein has been prepared for informational purposes only and is not intended to provide, and should not be relied on for investment, tax, accounting, or legal advice. No representation is being made as to whether any investment product, strategy, or security is suitable or appropriate for an investor’s particular circumstances. Assumptions, opinions, and forecasts herein constitute our judgment and are subject to change without notice.