International Equity Markets: Will This Performance Trend Continue?

Written by Sloan Smith, CAIA, CPWA® and Mark Elliott

After years of strong U.S. equity market performance, international stocks staged a meaningful comeback in 2025. Performance outside the U.S. was among the strongest in decades, raising the possibility that this shift could extend beyond just a single year. Today, many investors face a common challenge: U.S. equity markets are increasingly dominated by a small group of large-cap technology stocks called the Magnificent Seven (i.e., Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla), and portfolio returns have become tied to a narrow set of themes.[1] At the same time, the global economy is evolving. Interest rates are beginning to ease, governments outside the U.S. are increasing spending to support growth, and innovation from Artificial Intelligence (AI) to energy infrastructure is expanding well beyond U.S. borders. Furthermore, international equities are gaining attention due to their ability to diversify risk, broaden exposure, and reduce reliance on any single market or currency.

International equities provide exposure to different earnings cycles, sector mixes, policy frameworks, and currencies than those dominant in the U.S. They also address a core portfolio problem: concentrated risk in a handful of mega‑cap names and a single currency.[2] Non‑U.S. markets can offer access to diverse policy environments and long‑term investment in technology and infrastructure, particularly across emerging markets.

There were three broad developments that defined 2025:

Valuations adjusted upward. International markets entered 2025 priced at a discount relative to U.S. stocks. As economic conditions stabilized, investor confidence improved and prices more accurately reflected earnings potential.

Currency trends supported returns. A softer dollar increases the value of overseas holdings when converted back into U.S. currency and can also help foreign companies compete more effectively on the global stage, supporting returns for U.S.‑based investors.

Earnings expectations improved. Companies outside the U.S. generally exceeded lowered expectations, allowing returns to be supported by fundamentals rather than optimism alone.

Importantly, sentiment improved across global markets, with gains spreading beyond the narrow group of U.S. companies that had driven returns in prior years. These dynamics helped create real momentum heading into 2026. However, it is unknown whether this trend will continue, and it is important to weigh the advantages and potential risks of allocating to this asset class.

Advantages of Allocating to International Equities

Balanced Path to Returns. Investors can capture both earnings growth and valuation normalization in regions that still trade at discounts versus the U.S. market. Performance is likely to depend more on the ability of companies to consistently grow their earnings than on investors assigning higher valuation multiples.

Currency diversification. A less dominant U.S. dollar can support international returns and help spread currency risk across long‑term portfolios.

Portfolio balance. Reduces reliance on a small set of U.S. mega‑cap companies and introduces different sector and policy mixes, potentially mitigating drawdowns tied to U.S.-specific stocks.

Broader innovation. AI supply chains, data center and power capacity build‑outs, and energy transition projects are increasingly opening leadership beyond U.S. technology.

Risk of Allocating to International Equities

Currency risk. A stronger U.S. dollar could dilute returns and could tighten EM financial conditions.

Policy and geopolitical instability. Tariffs, regional conflicts, and shifting coalitions can disrupt trade, earnings visibility, and valuations.

Growth divergence risk. U.S. structural advantages could sustain U.S. outperformance versus parts of Europe and the Emerging Markets space.[3]

Manager and market selection. Market dispersion, governance standards, and sector quality vary widely in the international space. Execution matters in security and country selection.

Looking ahead, multiple factors may shape international equity performance, and the strength of corporate earnings is likely to be a primary driver as markets place greater emphasis on fundamental results rather than additional valuation gains. At the same time, the lagged effects of global monetary easing may support investment and consumption as lower rates filter through economies. These fundamentals are reinforced by ongoing capital allocation shifts, as investors reassess U.S. market concentration and valuation trade‑offs.

In response, many investors are positioning international exposure using developed international equities as a foundation and complementing them with selective emerging‑market allocations to enhance cyclicality and valuation diversification.[4] With U.S. market concentration elevated, policy support improving across regions, and innovation becoming increasingly global, international equities offer a structural response to today’s diversification and valuation challenges.

As the transition from 2025 to 2026 shifts market sentiment toward returns supported by earnings growth, investment spending, and broader participation, the case for a more balanced global equity allocation appears stronger than it has in years. Therefore, international equities seem positioned as a potential robust option for long‑horizon portfolios.

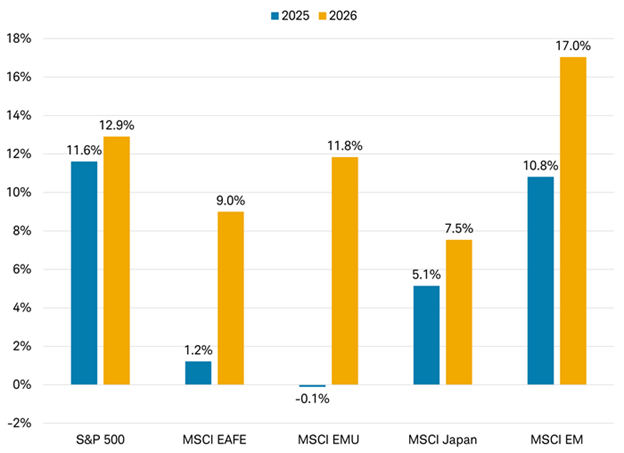

Figure 1: Estimates suggest international earnings growth could catch up with S&P 500 earnings growth

Source: Charles Schwab, “2026 Outlook: International Stocks and Economy.”

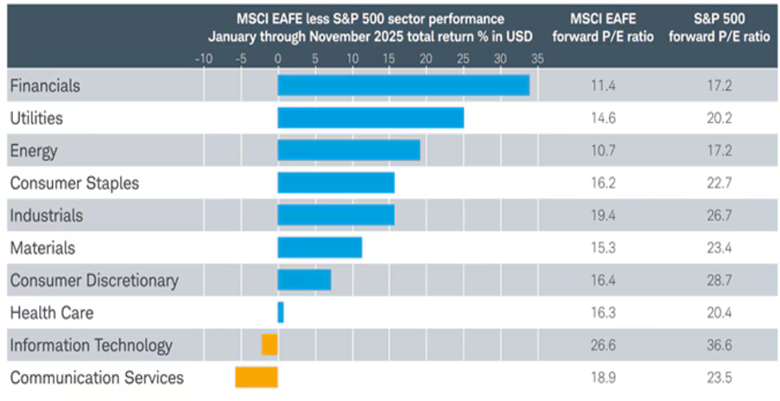

Figure 2: International equities are less expensive across every sector relative to the United States

Source: Charles Schwab, MSCI, Macrobond data retrieved 12/2/2025

[1] Source: Why Global Stocks are Not Yet in a Bubble, Goldman Sachs.

[2] Source: International Equities: Global Structural Changes Driving Narrowing U.S. Earnings Growth Exceptionalism, J.P Morgan.

[3] Source: U.S. Equity Outperformance in 2026: Structural Advantages from AI, Earnings Resilience, and Policy Tailwinds, Morgan Stanley.

[4] Source: Vanguard Economic and Market Outlook for 2026.