Fixed Income: The Value of an Active Investment Approach

Written by Sloan Smith, CAIA, CPWA® and Mark Elliott

The United States fixed income market has experienced significant volatility over the last six years. This trend initially started in 2020 during the COVID-19 pandemic when short-term interest rates went to zero percent, rose in 2022 to 5.25% - 5.5% in order to slow down rampant inflation, and then declined again to 3.5% to 3.75% after both inflation and unemployment moderated. At the same time, we saw the yield curve invert from 2022 to 2024, indicating a potential recession or slowdown in the economy, before quickly steepening throughout 2025. This movement in the fixed income market has been historic, but it provided tremendous opportunity for active fixed income investment managers who were thoughtful about security selection, duration, credit quality, and yield curve positioning. Going forward, the fixed income active management approach should continue to add value due to not only continued interest rate volatility but also the vast investment opportunities that are not found in typical benchmarks, such as the Bloomberg Barclays U.S. Aggregate Index.

The Index Trap: The Cost of Passive Exposure

The standard fixed income portfolio is often anchored to benchmarks like the Bloomberg Barclays U.S. Aggregate Index, which are fundamentally built on issuance-based weighting. This creates a structural "indebtedness bias" as an issuer accumulates more debt, its representation in the index increases. Consequently, passive strategies are mechanically forced to overweight the most leveraged entities, regardless of their underlying credit quality or valuation.

This lack of discernment is a significant performance headwind. Passive vehicles operate as "price-takers," bound to hold assets even as credit profiles deteriorate or as interest rate environments shift against them. This dynamic effectively turns a passive strategy into a reflection of past debt issuance rather than a forward-looking assessment of risk and return.

The Advantages of Active Management Fixed Income Management

By shifting away from the mentality of passive fixed income investing, active management offers distinct structural benefits such as the following:

Thoughtful Portfolio Shifts: Passive funds are mechanically bound to hold a bond until it is formally downgraded or matures. In contrast, an active manager can proactively exit a position the moment their research identifies fundamental credit deterioration. Also, active managers are able to adjust duration (interest rate sensitivity) and/or sector exposure based on evolving trends in the fixed income market.

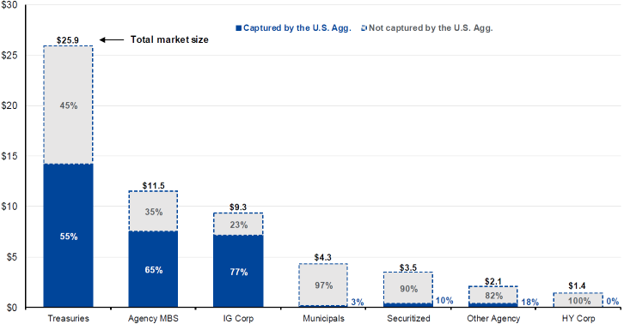

Access to the broader fixed income market: Traditional United States bond indices exclude nearly 48% of the broader fixed income landscape.[1] Active managers can traverse these "off-benchmark" areas, accessing sectors where market inefficiencies are higher and potential return profiles are often more robust.

Risk Mitigation: Because active managers are not bound by the index's "indebtedness bias," they can avoid systematically increasing exposure to the most highly leveraged issuers, effectively acting as a structural shock absorber for the portfolio.

Potential Risks

Manager Selection & Cost: Performance dispersion between top-quartile and bottom-quartile fixed income managers is wide, making it paramount to choose a high quality active fixed income strategy. Additionally, investors must weigh the higher management fees of active funds against lower fee options found in passive strategies.

Tracking Error & Liquidity: An active strategy may deviate from the broader market benchmark for extended periods, which can lead to greater tracking error. Also, investors must consider that in seeking off-benchmark opportunities, managers may venture into areas with lower liquidity.

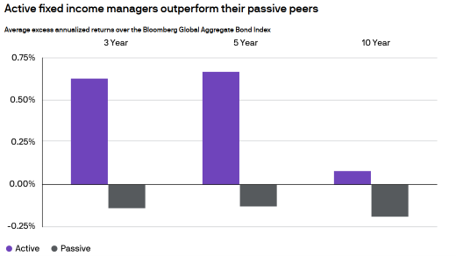

Active fixed income remains a robust solution for diversified portfolios. The asset class should function as an effective way to generate strong relative returns while substantially reducing downside risk in greater portfolios. Active strategies are able to rotate across different opportunities to ensure portfolios are not constrained by a potential interest rate, credit, or yield curve risks. Since the active investable universe is vast and varied, the goal is to outperform by identifying various inefficiencies and opportunities, which create consistent performance. Historically, all active fixed income funds have delivered 27 basis points of average annual excess return over the median passive peer group (net of fees), and outperformed in 64% of rolling 10-year periods as of 12/31/2025.[2] The dispersion in outcomes highlights that while the opportunity for active management is clear, the execution is grounded in rigorous, institutional-grade research and remains the true driver of long-term success.

In a market defined by volatility and divergent global trends, transitioning from passive fixed-income investing to active management allows investors to escape the "index trap" of forced debt exposure and instead employ tactical precision to prioritize capital preservation and consistent, risk-adjusted returns. The shift toward an active mandate is not a tactical bet against the market; it is a transition from passive reliance to active precision, representing a shift toward a more robust, diversified, and fundamentally sound approach to portfolio construction.

Figure 1

Fixed Income Investable Market vs. the Bloomberg U.S. Aggregate Index

USD trillions, 2Q25

[1] Source: Bank of America, Bloomberg, SIFMA, J.P. Morgan Asset Management.

Figure 2:

[2] Source: Pimco Fixed Income Insights