Missiles, Markets and Momentum: Why the Market Outlasts the Headlines

Written by Christian O’Dwyer, CFA and Brookyln Seymour

As tensions simmer between the United States, Israel, and Iran, markets once again find themselves caught between uncertainty and resilience. While the situation is fluid, it is part of a broader pattern of geopolitical friction in the Middle East. Historically, these tensions hit energy markets first and equities second, as oil prices quickly price in the risk of supply disruptions, particularly with critical chokepoints like the Strait of Hormuz. If we layer on top of that China’s dependence on Iranian oil, Russia’s ongoing war in Ukraine, and already elevated global tensions, we have a recipe for macroeconomic anxiety. Higher energy prices could act as a tax on growth, squeezing corporate margins, increasing transportation and manufacturing costs, complicating central bank policy and pressuring consumers worldwide. All of this is unfolding at a time when U.S. equity valuations are relatively high, leaving little room for error in the eyes of many investors. These dynamics put central banks like the Federal Reserve in a difficult position. The question posed is whether you support growth or remain restrictive to contain inflation? In a market priced for strong earnings and policy stability, any disruption to that balance can trigger sharp reactions. In this environment, geopolitics and energy prices have become key transmission mechanisms for volatility. What begins as a geopolitical event can quickly evolve into an economic narrative and, ultimately, a market repricing. In that context, geopolitical risk becomes not just a headline, but a meaningful catalyst for volatility.

And yet despite all of it the market has been doing remarkably well.

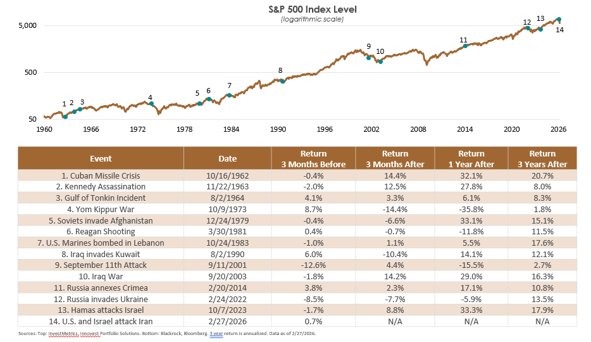

That’s the part that often feels counterintuitive. War headlines dominate the news cycle, but markets don’t operate purely on emotion. They digest information, reprice risk, and move forward. From the Cuban Missile Crisis to the Iraq War, from 9/11 to Russia’s invasion of Ukraine, the pattern is consistent. Markets may dip in the immediate aftermath, sometimes sharply, but they tend to recover and move higher over time. Even in the current environment, markets have demonstrated resilience. The S&P 500 has continued to reach new highs and post strong earnings growth despite ongoing geopolitical tensions tied to the Iran conflict. In fact, the average three-year return following major geopolitical events has been over 12%. That’s not a fluke, it reflects the adaptability of global economies, the resilience of corporate earnings, and the tendency for innovation and productivity to continue even in uncertain environments. Businesses adjust supply chains, governments implement policy responses, and capital flows to areas of opportunity. Over time, these forces compound, pushing markets higher. Another often overlooked dynamic is that geopolitical disruptions can create winners alongside losers. For example, higher energy prices can benefit U.S. energy producers and exporters, partially offsetting broader economic pressure. Energy stocks have outperformed the broader market by 25% year-to-date during the price surge. Markets are not static they evolve alongside the challenges they face.

This doesn’t mean risks should be ignored. A prolonged oil supply disruption, particularly involving Iran, could carry real consequences such as reviving inflation, slowing global growth, and leading to deeper or more sustained market drawdowns. Those risks are real, but volatility itself is not the exception in markets, it’s the rule. On average, the S&P 500 experiences a drawdown of about 14% every year, most of which occur without dramatic headlines. Yet over time, the market has continued to climb. Pullbacks of 5% happen multiple times per year on average, and corrections of 10% or more tend to occur roughly every 18 months. That’s why the most effective investment strategy remains consistent through wars, recessions, and political uncertainty: stay diversified, maintain a long-term perspective, and rebalance along the way. Successful compounding doesn’t require perfect timing; it requires discipline and patience.

Periods like this can feel especially tense, with higher stakes and more urgent headlines. Yet over time, markets have shown they are forward‑looking and resilient, absorbing uncertainty rather than freezing in it. While today’s geopolitical backdrop may feel unsettling, it fits a long history of disruptions that markets have ultimately navigated. The bottom line isn’t that risk doesn’t matter, it’s that long‑term perseverance tends to prevail.